Fill Out a Valid Broker Price Opinion Template

Form Specs

| Fact Name | Description |

|---|---|

| Purpose | A Broker Price Opinion (BPO) provides an estimate of a property's value, typically used in real estate transactions. |

| Components | The BPO form includes sections for market conditions, property details, and competitive listings. |

| Market Conditions | It assesses current market conditions, including employment trends and pricing changes. |

| Subject Property | The form requires detailed information about the subject property, such as its condition and type. |

| Comparable Sales | It includes a section for comparing the subject property with similar properties that have recently sold. |

| Marketing Strategy | The BPO outlines a marketing strategy, indicating whether the property will be sold as-is or repaired. |

| Repairs | It lists necessary repairs to make the property marketable, along with associated costs. |

| Market Value | The BPO provides a suggested market value based on competitive closed sales. |

| State-Specific Forms | Some states have specific regulations governing BPOs. Always check local laws. |

| Signature Requirement | A signature is required to validate the BPO, confirming the information is accurate and complete. |

Dos and Don'ts

When filling out the Broker Price Opinion form, follow these guidelines to ensure accuracy and professionalism.

- Do provide complete and accurate information for all sections.

- Do use current market data to support your assessments.

- Do clearly indicate any repairs needed for the property.

- Do include all relevant comparable sales data.

- Don't leave any fields blank unless absolutely necessary.

- Don't exaggerate property features or market conditions.

- Don't forget to sign and date the form upon completion.

- Don't rely on outdated or irrelevant data for your evaluations.

Other PDF Documents

Stem Opt Employer Requirements - Students are encouraged to have discussions with their employers while drafting the I-983.

Understanding the importance of the WC-240 form is essential for both employers and employees in Georgia's workers' compensation landscape. This form not only serves as a legal requirement but also facilitates a smooth transition back to work by clearly outlining job offers that align with the employee's medical capabilities. For more information, you can visit georgiaform.com, which provides resources and guidance on navigating these processes effectively.

Credit Application Business - Our goal is to assist you in growing your business successfully.

Common mistakes

-

Incomplete Information: Failing to fill in all required fields can lead to delays and misunderstandings. Each section, from the property address to the sales representative’s name, is crucial for accurate assessment.

-

Incorrect Market Conditions: Misrepresenting current market conditions can skew the valuation. It’s essential to accurately assess whether the market is depressed, stable, or improving.

-

Neglecting Comparable Listings: Not providing sufficient comparable sales data can undermine the credibility of the opinion. A thorough analysis of nearby properties is vital for an accurate valuation.

-

Ignoring Property Condition: Underestimating the impact of the property's condition can lead to inaccurate pricing. Clearly stating whether the property is in excellent, fair, or poor condition is necessary.

-

Omitting Financing Information: Failing to specify available financing options can mislead potential buyers. It’s important to clarify whether all types of financing are available or if there are restrictions.

-

Inaccurate Adjustments: Making errors in value adjustments for comparable properties can distort the final price opinion. Each adjustment should be carefully calculated and justified.

-

Not Considering Repairs: Overlooking necessary repairs can misrepresent the property's marketability. Listing all required repairs helps provide a clearer picture of the property’s true value.

-

Failure to Comment on Special Concerns: Not addressing specific issues like encroachments or environmental concerns can lead to future complications. Detailed comments are essential for transparency.

Documents used along the form

The Broker Price Opinion (BPO) form is a vital document in real estate transactions, particularly for determining property values. When using a BPO, several other forms and documents often accompany it to provide a comprehensive view of the property and its market conditions. Here’s a list of commonly used forms that complement the BPO.

- Comparative Market Analysis (CMA): A CMA is a report that evaluates similar properties in the area to determine a competitive price for a property. It includes data on recently sold homes, active listings, and properties that failed to sell, offering a broader context for the BPO.

- Property Condition Report: This document details the physical condition of the property, including any repairs needed. It helps to identify issues that may affect the property's value and marketability, providing essential information for the BPO.

- Listing Agreement: A listing agreement is a contract between the property owner and the real estate broker. It outlines the terms of the listing, including the duration, commission, and responsibilities of both parties, ensuring clarity in the sales process.

- Vehicle/Vessel Transfer and Reassignment Form: Essential for the transfer of ownership in California, the https://californiadocsonline.com/california-fotm-reg-262-form/ must accompany the title or application for a duplicate title to ensure compliance with state laws and protect the rights of both buyers and sellers.

- Sales Disclosure Form: This form is often required by law and provides buyers with important information about the property’s condition, including any known defects or issues. It ensures transparency and helps protect both the buyer and seller during the transaction.

Using these forms alongside the Broker Price Opinion can enhance the understanding of the property’s value and condition. Together, they create a well-rounded picture that benefits all parties involved in the real estate process.

Misconceptions

Understanding the Broker Price Opinion (BPO) form can be challenging, and several misconceptions often arise. Here are nine common misunderstandings about the BPO form, along with clarifications to help demystify the process.

-

Misconception 1: The BPO is the same as an appraisal.

While both documents assess property value, a BPO is generally less formal and is often used for quicker evaluations, while an appraisal is more comprehensive and regulated.

-

Misconception 2: A BPO is only used for foreclosures.

This is not true. A BPO can be utilized in various situations, including short sales, refinancing, and determining market value for sales.

-

Misconception 3: The BPO is always accurate.

Accuracy can vary based on the information provided and the market conditions. It is an opinion based on available data and should be viewed as a guideline rather than a definitive value.

-

Misconception 4: Only real estate agents can complete a BPO.

While licensed real estate agents typically prepare BPOs, other qualified professionals may also provide this service, depending on state regulations.

-

Misconception 5: A BPO is a lengthy process.

In many cases, a BPO can be completed relatively quickly, often within a few days, depending on the complexity of the property and the local market.

-

Misconception 6: The BPO form is too complicated to understand.

Though the form contains various sections, each is designed to gather essential information about the property and market conditions. With some familiarity, it becomes easier to navigate.

-

Misconception 7: A BPO guarantees a sale price.

A BPO provides an estimated value but does not guarantee that the property will sell for that amount. Market fluctuations and buyer interest can significantly influence the final sale price.

-

Misconception 8: The BPO does not consider neighborhood conditions.

In fact, the BPO form includes sections dedicated to assessing neighborhood conditions, such as market trends and the presence of comparable properties.

-

Misconception 9: Once completed, a BPO cannot be updated.

On the contrary, BPOs can be updated as market conditions change or if new information about the property becomes available. Regular updates can provide a more accurate reflection of the property's value.

By addressing these misconceptions, individuals can better understand the purpose and utility of the Broker Price Opinion form. This knowledge can empower homeowners, buyers, and real estate professionals alike.

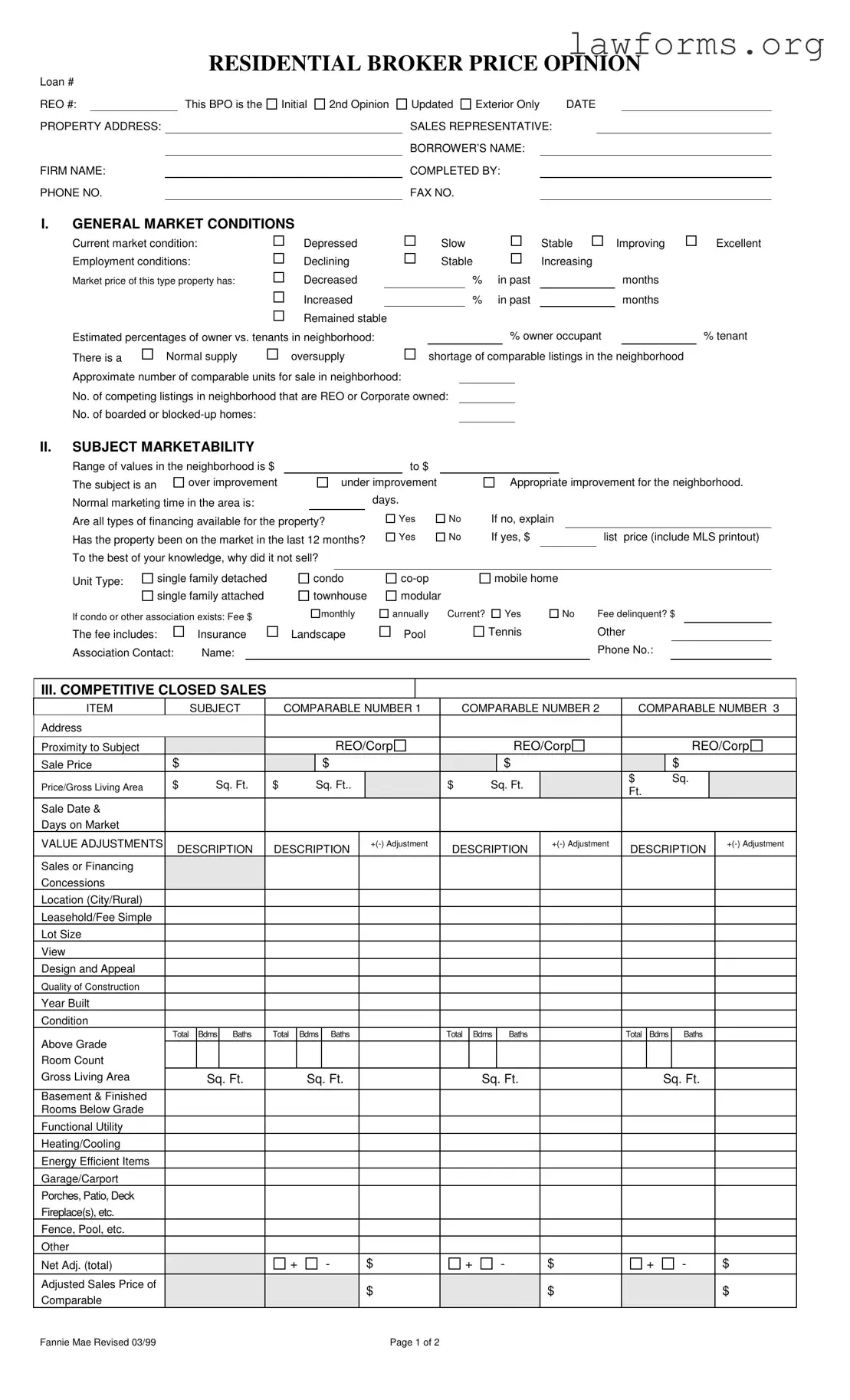

Preview - Broker Price Opinion Form

RESIDENTIAL BROKER PRICE OPINION

Loan #

REO #:This BPO is the

PROPERTY ADDRESS:

FIRM NAME:

PHONE NO.

Initial

2nd Opinion

Updated Exterior Only |

DATE |

|||

SALES REPRESENTATIVE: |

|

|

|

|

BORROWER’S NAME: |

|

|

|

|

COMPLETED BY: |

|

|

|

|

FAX NO. |

|

|

|

|

I.GENERAL MARKET CONDITIONS

Current market condition: |

Depressed |

Slow |

|

Stable |

Improving |

||

Employment conditions: |

Declining |

Stable |

|

Increasing |

|

||

Market price of this type property has: |

Decreased |

|

|

% |

in past |

|

months |

|

Increased |

|

|

% |

in past |

|

months |

|

Remained stable |

|

|

|

|

|

|

Estimated percentages of owner vs. tenants in neighborhood: |

|

|

% owner occupant |

|

|||

There is a |

Normal supply |

oversupply |

shortage of comparable listings in the neighborhood |

||||

Approximate number of comparable units for sale in neighborhood: |

|

|

|

|

|

||

No. of competing listings in neighborhood that are REO or Corporate owned:

No. of boarded or

Excellent

% tenant

II.SUBJECT MARKETABILITY

Range of values in the neighborhood is $ |

|

|

|

|

|

to $ |

|

|

|

|

|

|

|

|

The subject is an |

over improvement |

|

|

under improvement |

|

Appropriate improvement for the neighborhood. |

||||||||

Normal marketing time in the area is: |

|

|

|

|

days. |

|

|

|

|

|

|

|||

Are all types of financing available for the property? |

Yes |

No |

If no, explain |

|

|

|

||||||||

Has the property been on the market in the last 12 months? |

Yes |

No |

If yes, $ |

|

|

list price (include MLS printout) |

||||||||

To the best of your knowledge, why did it not sell? |

|

|

|

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

||||

Unit Type: |

single family detached |

|

condo |

|

mobile home |

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

single family attached |

|

townhouse |

modular |

|

|

|

|

|

|

||||

If condo or other association exists: Fee $

monthly

annually Current?

Yes

No |

Fee delinquent? $ |

The fee includes:

Association Contact:

Insurance

Name:

Landscape

Pool

Tennis |

Other |

|

Phone No.: |

III. COMPETITIVE CLOSED SALES

ITEM |

|

|

SUBJECT |

|

COMPARABLE NUMBER 1 |

|

COMPARABLE NUMBER 2 |

|

COMPARABLE NUMBER 3 |

|||||||||||||||||||||||

Address |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Proximity to Subject |

|

|

|

|

|

|

|

|

|

|

REO/Corp |

|

|

|

|

|

|

REO/Corp |

|

|

|

|

|

REO/Corp |

||||||||

Sale Price |

$ |

|

|

|

|

|

|

$ |

|

|

|

|

|

|

|

|

|

$ |

|

|

|

|

|

|

|

$ |

|

|

|

|||

Price/Gross Living Area |

$ |

|

Sq. Ft. |

$ |

|

Sq. Ft.. |

|

|

$ |

|

|

Sq. Ft. |

|

|

$ |

|

|

|

Sq. |

|

|

|

||||||||||

|

|

|

|

|

|

|

|

|

Ft. |

|

|

|

|

|||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

Sale Date & |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Days on Market |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

VALUE ADJUSTMENTS |

|

DESCRIPTION |

|

DESCRIPTION |

|

|

DESCRIPTION |

|

DESCRIPTION |

|

||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||||||

Sales or Financing |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Concessions |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Location (City/Rural) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Leasehold/Fee Simple |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Lot Size |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

View |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Design and Appeal |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Quality of Construction |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Year Built |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Condition |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Total |

|

Bdms |

Baths |

|

Total |

Bdms |

|

Baths |

|

|

|

Total |

|

Bdms |

|

Baths |

|

|

Total |

Bdms |

Baths |

|

|

|

||||||

Above Grade |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Room Count |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Gross Living Area |

|

|

|

Sq. Ft. |

|

|

Sq. Ft. |

|

|

|

|

|

|

Sq. Ft. |

|

|

|

|

|

Sq. Ft. |

|

|

|

|||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Basement & Finished |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Rooms Below Grade |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Functional Utility |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Heating/Cooling |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Energy Efficient Items |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Garage/Carport |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Porches, Patio, Deck |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Fireplace(s), etc. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Fence, Pool, etc. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Other |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Net Adj. (total) |

|

|

|

|

|

+ |

- |

|

|

$ |

|

+ |

- |

|

$ |

|

+ |

|

|

- |

|

$ |

|

|||||||||

Adjusted Sales Price of |

|

|

|

|

|

|

|

|

|

|

|

|

$ |

|

|

|

|

|

|

|

|

$ |

|

|

|

|

|

|

|

|

$ |

|

Comparable |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Fannie Mae Revised 03/99 |

|

|

|

|

|

|

|

|

|

|

|

|

Page 1 of 2 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

REO# |

Loan # |

IV. MARKETING STRATEGY

Minimal Lender Required Repairs |

V. REPAIRS

Occupancy Status: Occupied

Repaired Most Likely Buyer:

Vacant

Unknown

Unknown

Owner occupant

Investor

Investor

Itemize ALL repairs needed to bring property from its present “as is” condition to average marketable condition for the neighborhood. Check those repairs you recommend that we perform for most successful marketing of the property.

$

$

$

$

$

$

$

$

$

$

|

|

|

|

GRAND TOTAL FOR ALL REPAIRS $ |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

VI. COMPETITIVE LISTINGS |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

ITEM |

|

|

SUBJECT |

COMPARABLE NUMBER 1 |

COMPARABLE NUMBER. 2 |

COMPARABLE NUMBER. 3 |

|||||||||||||||||||||

Address |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Proximity to Subject |

|

|

|

|

|

REO/Corp |

|

|

|

|

|

REO/Corp |

|

|

REO/Corp |

||||||||||||

List Price |

$ |

|

|

|

|

|

|

$ |

|

|

|

|

|

|

|

$ |

|

|

|

|

|

|

$ |

|

|

||

Price/Gross Living Area |

$ |

|

Sq.Ft. |

$ |

Sq.Ft. |

|

|

|

$ |

Sq.Ft. |

|

|

|

$ |

Sq.Ft. |

|

|

||||||||||

Data and/or |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Verification Sources |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

VALUE ADJUSTMENTS |

|

DESCRIPTION |

DESCRIPTION |

|

+ |

DESCRIPTION |

|

DESCRIPTION |

|||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Sales or Financing |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Concessions |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Days on Market and |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Date on Market |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Location (City/Rural) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Leasehold/Fee |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Simple |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Lot Size |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

View |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Design and Appeal |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Quality of Construction |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Year Built |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Condition |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Above Grade |

Total |

Bdms |

Baths |

Total |

Bdms |

Baths |

|

|

|

Total |

Bdms |

|

Baths |

|

Total |

Bdms |

|

Baths |

|

|

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Room Count |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Gross Living Area |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

Sq. Ft. |

|

Sq. Ft. |

|

|

|

Sq. Ft. |

|

|

|

Sq. Ft. |

|

|

|||||||||||||

Basement & Finished |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Rooms Below Grade |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Functional Utility |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Heating/Cooling |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Energy Efficient Items |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Garage/Carport |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Porches, Patio, Deck |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Fireplace(s), etc. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Fence, Pool, etc. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Other |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

Net Adj. (total) |

|

|

|

|

+ |

- |

|

|

|

$ |

|

|

+ |

- |

- |

|

$ |

|

|

+ |

- |

|

$ |

|

|

||

Adjusted Sales Price |

|

|

|

|

|

|

|

|

|

$ |

|

|

|

|

|

|

|

$ |

|

|

|

|

|

|

$ |

|

|

of Comparable |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

VI. THE MARKET VALUE (The value must fall within the indicated value of the Competitive Closed Sales).

Market Value |

Suggested List Price |

AS IS REPAIRED

30 Quick Sale Value

Last Sale of Subject, Price |

Date |

COMMENTS (Include specific positives/negatives, special concerns, encroachments, easements, water rights, environmental concerns, flood zones, etc. Attach addendum if additional space is needed.)

Signature: |

|

Date: |

Fannie Mae Revised 03/99 |

Page 2 of 2 |

CMS Publishing Company 1 800 |

Key takeaways

Filling out and utilizing the Broker Price Opinion (BPO) form is crucial for accurately assessing property values. Here are some key takeaways to keep in mind:

- Understand Market Conditions: It's essential to evaluate the current market conditions, including employment rates and the number of comparable listings. This information helps provide context for the property's value.

- Accurate Comparables: When selecting comparable properties, ensure they are similar in size, location, and condition. This will enhance the reliability of your price opinion.

- Detail Necessary Repairs: Clearly itemize any repairs needed to bring the property to marketable condition. This transparency can influence potential buyers and lenders.

- Provide Comprehensive Comments: Use the comments section to highlight any unique features or concerns about the property. This can include environmental issues or specific neighborhood attributes that may impact value.

Similar forms

- Comparative Market Analysis (CMA): Similar to a Broker Price Opinion, a CMA assesses the value of a property by comparing it to similar properties that have recently sold in the area. Both documents provide insights into market conditions and property values.

- Appraisal Report: An appraisal report offers a professional opinion of a property's value, often conducted by a licensed appraiser. Like a BPO, it considers comparable sales, but appraisals are usually more detailed and formal.

- Listing Agreement: A listing agreement is a contract between a property owner and a real estate agent. While it does not estimate value, it often references market conditions and the anticipated price range, similar to what is outlined in a BPO.

- Purchase Agreement: This document outlines the terms of a property sale, including price. It reflects the market value indicated in a BPO, as both aim to establish a fair price based on current market conditions.

- Market Analysis Report: A market analysis report provides a broader overview of market trends and conditions. It shares similarities with a BPO by offering insights into property values and market dynamics.

- Investment Analysis: This document evaluates the potential return on investment for a property. Like a BPO, it considers market conditions and property values, but focuses more on financial metrics and investment viability.

- Property Condition Report: A property condition report details the physical state of a property. While it does not provide a value, it complements a BPO by addressing factors that may influence marketability and pricing.

- Residential Lease Agreement: The Ohio PDF Forms can be utilized to create a comprehensive residential lease agreement, ensuring that both landlords and tenants have a clear understanding of their rights and responsibilities in the rental relationship.

- Real Estate Market Report: This report analyzes trends in the real estate market, including pricing and sales activity. It aligns with a BPO in its focus on current market conditions and property values.