Fill Out a Valid Cg 20 10 07 04 Liability Endorsement Template

Form Specs

| Fact Name | Details |

|---|---|

| Policy Number | CG 20 10 12 19 |

| Purpose | This endorsement adds additional insured status for owners, lessees, or contractors. |

| Coverage Modification | It modifies the insurance provided under the Commercial General Liability Coverage Part. |

| Liability Scope | Covers liability for bodily injury, property damage, or personal and advertising injury caused by the named insured's actions or omissions. |

| Exclusions | Coverage does not apply after all work on the project has been completed or if the work has been put to its intended use. |

| Insurance Limits | The maximum payout is the lesser of the contract-required amount or the applicable insurance limits. |

| Governing Laws | State-specific laws may apply; check local regulations for additional requirements. |

Dos and Don'ts

When filling out the CG 20 10 07 04 Liability Endorsement form, it's essential to be thorough and accurate. Here are ten tips to help you navigate the process effectively:

- Do read the form carefully before starting to fill it out.

- Do ensure you have the correct policy number at hand.

- Do list all additional insured persons or organizations clearly.

- Do specify the location of covered operations accurately.

- Do double-check for any required information that may not be shown above.

- Don't leave any sections blank unless explicitly stated as optional.

- Don't provide information that is not relevant to the endorsement.

- Don't forget to review the exclusions that apply to the additional insureds.

- Don't assume coverage without verifying the terms of your contract.

- Don't submit the form without a final review for errors or omissions.

Other PDF Documents

Miscellaneous Information - The form highlights the importance of thorough record-keeping for tax purposes.

Affidavit of Custody - Revoking the relinquishment is possible within 11 days, but must follow specific procedures.

When engaging in activities requiring a waiver of liability, it's essential to understand the nuances of legal agreements like the Washington Hold Harmless Agreement. This document is vital for protecting parties from potential claims of damages or injuries during specific events or activities. For those looking to draft a comprehensive agreement, resources such as Forms Washington can provide valuable templates and guidance.

Electrical Panel Schedule Template - Document any changes in the electrical panel configuration.

Common mistakes

-

Incomplete Information: Failing to provide all necessary details, such as the names of additional insured persons or organizations, can lead to significant coverage gaps.

-

Incorrect Policy Number: Entering the wrong policy number can cause confusion and delays in processing the endorsement, potentially leaving you unprotected.

-

Misunderstanding Coverage Limits: Not fully understanding the limits of insurance can result in expectations that exceed what is actually provided, especially in contractual situations.

-

Neglecting to Review Exclusions: Ignoring the specific exclusions listed in the endorsement may lead to unexpected denials of claims, particularly regarding the timing of when coverage applies.

-

Omitting Required Signatures: Failing to sign the form or obtain necessary signatures from all parties involved can render the endorsement invalid.

-

Assuming Automatic Coverage: Assuming that additional insured status automatically applies without confirming contractual obligations can lead to misunderstandings and inadequate protection.

Documents used along the form

The CG 20 10 07 04 Liability Endorsement form is commonly used in conjunction with several other documents that support liability coverage and clarify the terms of insurance policies. Each of these documents serves a specific purpose in the context of commercial general liability insurance.

- Commercial General Liability (CGL) Policy: This is the primary insurance policy that provides coverage for bodily injury, property damage, and personal injury claims. It outlines the overall terms and conditions of coverage.

- Minnesota Motor Vehicle Bill of Sale – This important document records the transfer of a vehicle from one person to another, safeguarding the interests of both seller and buyer. For more information, you can refer to Formaid Org.

- Certificate of Insurance: This document serves as proof of insurance coverage. It provides details about the policy, including coverage limits and the insured parties, and is often required by clients or partners.

- Additional Insured Endorsement: Similar to the CG 20 10 07 04 form, this endorsement adds another party as an insured under the policy, extending coverage to them for specific liabilities related to the insured's operations.

- Contractual Liability Endorsement: This endorsement modifies the policy to cover liabilities assumed under contracts. It clarifies the extent of coverage for obligations taken on through contractual agreements.

- Waiver of Subrogation Endorsement: This document prevents the insurer from pursuing recovery from a third party after paying a claim. It is often included in contracts to protect relationships between parties.

- Exclusion Endorsements: These documents specify certain risks or situations that are not covered by the policy. They help define the limits of liability and clarify what is excluded from coverage.

- Declarations Page: This page summarizes the key details of the insurance policy, including coverage limits, deductibles, and the parties involved. It is often referenced in conjunction with other forms.

- Loss Run Reports: These reports provide a history of claims made under the policy. They are used by underwriters to assess risk and determine future premiums.

- Indemnity Agreement: This is a contract in which one party agrees to compensate another for certain damages or losses. It is often linked to the additional insured status and outlines the responsibilities of each party.

Understanding these documents and their interrelation with the CG 20 10 07 04 Liability Endorsement form is crucial for managing liability risks effectively. Each document plays a role in defining the scope of coverage and ensuring compliance with contractual obligations.

Misconceptions

Here are ten common misconceptions about the CG 20 10 07 04 Liability Endorsement form, along with clarifications for each:

- This endorsement automatically covers all parties involved. The endorsement only covers the specific additional insureds listed in the schedule. It does not extend coverage to all parties by default.

- All types of liability are covered. The endorsement specifically covers liability for "bodily injury," "property damage," or "personal and advertising injury" caused by your actions or those acting on your behalf. Other types of liability may not be included.

- Coverage applies regardless of the contract terms. If coverage for the additional insured is required by a contract, it will not exceed the terms of that contract. This means the endorsement is limited to what the contract specifies.

- The endorsement provides unlimited coverage. The limits of insurance remain unchanged by this endorsement. The coverage is subject to the limits of the policy or the contract, whichever is less.

- Work completed by the additional insured is covered. The endorsement does not cover "bodily injury" or "property damage" occurring after all work related to the project has been completed. This includes materials and equipment.

- It covers all operations at any location. Coverage is only applicable to the specific operations and locations designated in the endorsement. It does not apply to all activities or locations.

- All subcontractors are automatically covered. Only the additional insureds listed in the endorsement are covered. Subcontractors may not have coverage unless specifically included.

- Insurance applies to all injuries or damages. The endorsement limits coverage to injuries or damages directly resulting from your operations for the additional insureds. Other claims may not be covered.

- Once the work is done, coverage continues indefinitely. Coverage ends once the work has been completed or the project has been put to its intended use by someone other than another contractor or subcontractor.

- This endorsement increases the policy limits. The endorsement does not increase the applicable limits of insurance. It simply extends coverage to the additional insureds as specified.

Understanding these misconceptions can help clarify the coverage and limitations of the CG 20 10 07 04 Liability Endorsement form. It is crucial to read the endorsement carefully and consult with a professional if you have questions.

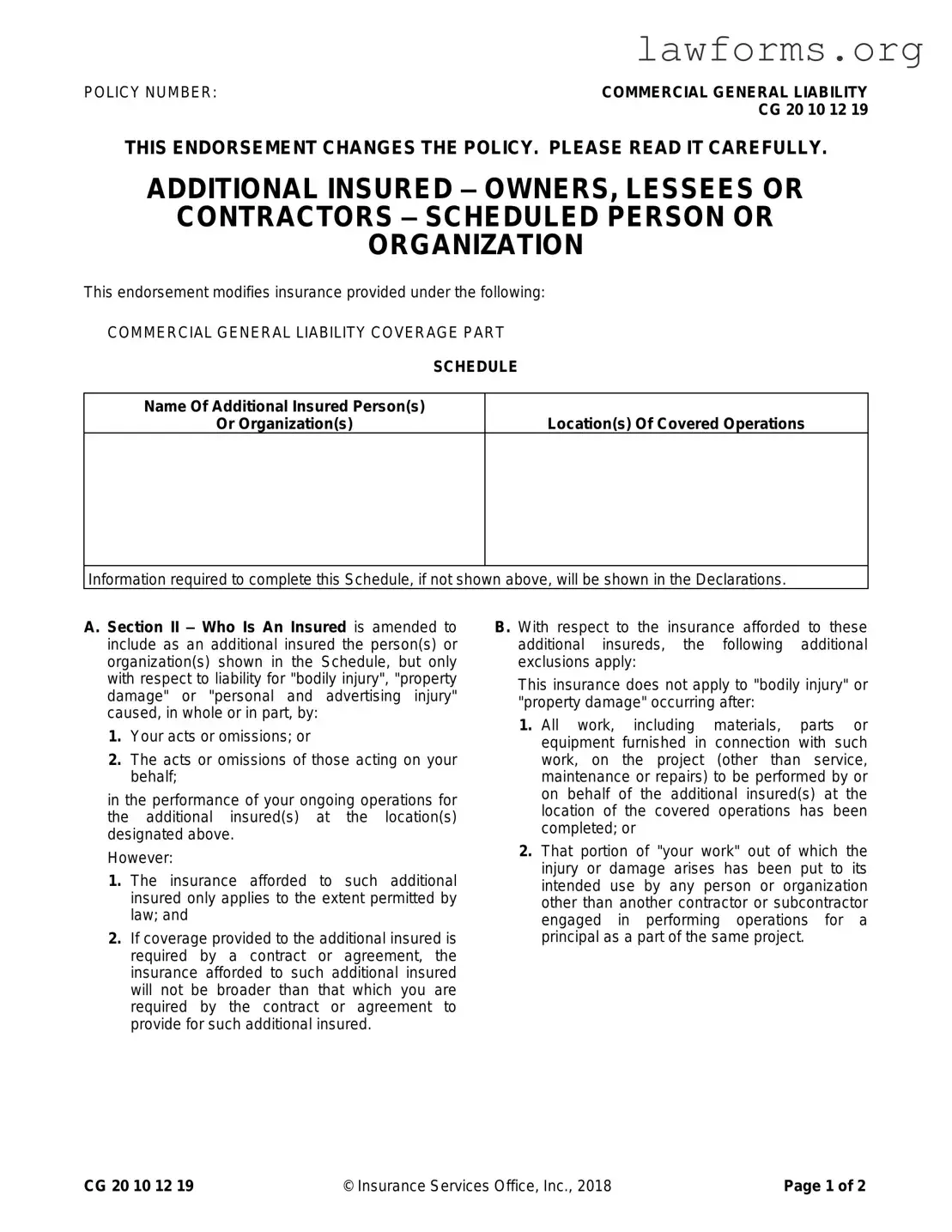

Preview - Cg 20 10 07 04 Liability Endorsement Form

POLICY NUMBER: |

COMMERCIAL GENERAL LIABILITY |

|

CG 20 10 12 19 |

THIS ENDORSEMENT CHANGES THE POLICY. PLEASE READ IT CAREFULLY.

ADDITIONAL INSURED – OWNERS, LESSEES OR

CONTRACTORS – SCHEDULED PERSON OR

ORGANIZATION

This endorsement modifies insurance provided under the following:

COMMERCIAL GENERAL LIABILITY COVERAGE PART

SCHEDULE

Name Of Additional Insured Person(s)

Or Organization(s)

Location(s) Of Covered Operations

Information required to complete this Schedule, if not shown above, will be shown in the Declarations.

A. Section II – Who Is An Insured is amended to include as an additional insured the person(s) or organization(s) shown in the Schedule, but only with respect to liability for "bodily injury", "property damage" or "personal and advertising injury" caused, in whole or in part, by:

1.Your acts or omissions; or

2.The acts or omissions of those acting on your behalf;

in the performance of your ongoing operations for the additional insured(s) at the location(s) designated above.

However:

1.The insurance afforded to such additional insured only applies to the extent permitted by law; and

2.If coverage provided to the additional insured is required by a contract or agreement, the insurance afforded to such additional insured will not be broader than that which you are required by the contract or agreement to provide for such additional insured.

B. With respect to the insurance afforded to these additional insureds, the following additional exclusions apply:

This insurance does not apply to "bodily injury" or "property damage" occurring after:

1.All work, including materials, parts or equipment furnished in connection with such work, on the project (other than service, maintenance or repairs) to be performed by or on behalf of the additional insured(s) at the location of the covered operations has been completed; or

2.That portion of "your work" out of which the injury or damage arises has been put to its intended use by any person or organization other than another contractor or subcontractor engaged in performing operations for a principal as a part of the same project.

CG 20 10 12 19 |

© Insurance Services Office, Inc., 2018 |

Page 1 of 2 |

C. With respect to the insurance afforded to these additional insureds, the following is added to

Section III – Limits Of Insurance:

If coverage provided to the additional insured is required by a contract or agreement, the most we will pay on behalf of the additional insured is the amount of insurance:

1.Required by the contract or agreement; or

2.Available under the applicable limits of insurance;

whichever is less.

This endorsement shall not increase the applicable limits of insurance.

Page 2 of 2 |

© Insurance Services Office, Inc., 2018 |

CG 20 10 12 19 |

Key takeaways

When filling out and using the CG 20 10 07 04 Liability Endorsement form, keep these key takeaways in mind:

- Policy Number: Ensure you have the correct policy number for your Commercial General Liability coverage.

- Additional Insured: Clearly list the names of any additional insured persons or organizations in the designated section.

- Location Details: Specify the locations where the coverage applies to avoid confusion later.

- Coverage Scope: Understand that the coverage is limited to liability for bodily injury, property damage, or personal and advertising injury.

- Acts and Omissions: Coverage applies to your actions or those acting on your behalf during ongoing operations for the additional insured.

- Legal Limits: The insurance provided is subject to the limits permitted by law.

- Contractual Obligations: If a contract requires additional insured coverage, it cannot exceed what is stipulated in that contract.

- Exclusions: Be aware that coverage does not apply if the work has been completed or if the injury arises after the work has been put to its intended use.

- Limits of Insurance: The maximum amount payable on behalf of the additional insured is the lesser of the contract requirement or the available limits of insurance.

- No Increase in Limits: This endorsement does not increase the overall limits of your insurance policy.

By following these guidelines, you can effectively navigate the CG 20 10 07 04 Liability Endorsement form and ensure proper coverage for your additional insureds.

Similar forms

CG 20 10 11 01 – Additional Insured – Owners, Lessees or Contractors – Automatic Status When Required in Written Contract: This form automatically includes additional insureds when required by a written contract. Similar to the CG 20 10 07 04, it provides coverage for liability arising from the named insured's operations, but it does not require a specific schedule of additional insureds.

CG 20 10 09 01 – Additional Insured – Owners, Lessees or Contractors – Scheduled Person or Organization: Like the CG 20 10 07 04, this endorsement allows for the addition of specific individuals or organizations as additional insureds. The coverage applies to liability resulting from the named insured's operations, emphasizing the importance of the scheduled parties.

California Durable Power of Attorney: Essential for anyone planning for the future, this form allows the principal to appoint an agent to manage their financial and legal matters, even during incapacitation, which can be crucial for ensuring wishes are followed. For more information, visit https://californiadocsonline.com/durable-power-of-attorney-form.

CG 20 37 04 13 – Additional Insured – Designated Person or Organization: This endorsement is similar in that it adds specific individuals or organizations as additional insureds. However, it is often used for more specialized circumstances, such as specific projects or contracts.

CG 20 10 10 01 – Additional Insured – Owners, Lessees or Contractors – Completed Operations: This form provides coverage for additional insureds specifically related to completed operations. It shares similarities with the CG 20 10 07 04 by addressing liability but focuses on incidents occurring after work has been completed.

CG 20 11 04 13 – Additional Insured – Joint Venture: This endorsement is used when multiple parties are involved in a joint venture. It provides coverage to additional insureds similar to the CG 20 10 07 04, ensuring that all parties are protected against liability arising from the joint venture's operations.

CG 20 10 14 13 – Additional Insured – Managers or Lessors of Premises: This form extends coverage to property managers or lessors, akin to the CG 20 10 07 04. It addresses liability arising from the named insured's operations but is specific to premises-related risks.