Valid Deed in Lieu of Foreclosure Form

State-specific Deed in Lieu of Foreclosure Documents

Form Specifications

| Fact Name | Description |

|---|---|

| Definition | A Deed in Lieu of Foreclosure is a legal document where a homeowner voluntarily transfers ownership of their property to the lender to avoid foreclosure. |

| Purpose | This process helps homeowners mitigate the negative impact of foreclosure on their credit score. |

| Eligibility | Homeowners must typically be in default on their mortgage payments to qualify for this option. |

| State-Specific Forms | Many states have specific forms and requirements for Deeds in Lieu. For example, California requires compliance with Civil Code Section 2924. |

| Tax Implications | Homeowners may face tax consequences, as the IRS may consider forgiven debt as taxable income. |

| Negotiation | Homeowners can negotiate terms with the lender, including potential relocation assistance. |

| Impact on Credit | While a Deed in Lieu is less damaging than foreclosure, it can still negatively affect credit scores. |

| Legal Advice | Consulting a legal advisor is recommended to understand rights and obligations before proceeding. |

| Alternative Options | Homeowners may also explore alternatives like loan modifications or short sales before opting for a Deed in Lieu. |

Dos and Don'ts

When filling out the Deed in Lieu of Foreclosure form, it is important to follow certain guidelines to ensure the process goes smoothly. Here are five things you should and shouldn't do:

- Do ensure that all information is accurate and complete. Double-check names, addresses, and property details.

- Do consult with a legal advisor or real estate professional if you have any questions about the form.

- Do provide any required documentation, such as proof of hardship or financial statements, to support your request.

- Don't rush through the process. Take your time to review the form thoroughly before submission.

- Don't sign the document without understanding the implications of a Deed in Lieu of Foreclosure.

Create Popular Types of Deed in Lieu of Foreclosure Documents

United States Tod - It allows individuals to provide for loved ones while retaining complete control over their property during their lifetime.

Free Lady Bird Deed Form - A Lady Bird Deed often requires less formalities than traditional wills, making it a user-friendly option.

For those navigating end-of-life decisions, understanding the implications of a Do Not Resuscitate Order for patients in Texas can be crucial. This document helps ensure that your medical preferences are honored, allowing peace of mind in difficult times.

California Corrective Deed - Utilizing this form can prevent potential litigation over ownership disputes.

Common mistakes

-

Not Understanding the Process: Many individuals jump into filling out the form without fully grasping what a deed in lieu of foreclosure entails. It's crucial to understand that this process involves voluntarily transferring property ownership to the lender to avoid foreclosure.

-

Incomplete Information: Failing to provide all required information can delay the process. Ensure that all fields are filled out accurately, including names, addresses, and loan details.

-

Ignoring Outstanding Liens: Some people overlook existing liens on the property. All liens must be addressed before proceeding, as they can complicate the transfer.

-

Not Seeking Legal Advice: Skipping the step of consulting a legal professional can lead to misunderstandings. Legal advice can clarify rights and obligations before signing any documents.

-

Failing to Communicate with the Lender: Lack of communication with the lender can lead to confusion. It's essential to stay in contact and clarify any requirements they may have.

-

Not Considering Tax Implications: Many individuals forget to consider potential tax consequences. Transferring property may have tax implications that need to be understood beforehand.

-

Overlooking the Condition of the Property: The condition of the property can affect the lender's acceptance. Ensure that the property is in a reasonable condition to avoid complications.

-

Not Keeping Copies of Documents: Failing to retain copies of all submitted documents can lead to issues later. Always keep a record for your personal files.

Documents used along the form

A Deed in Lieu of Foreclosure is a legal agreement that allows a homeowner to voluntarily transfer ownership of their property to the lender to avoid foreclosure. This process can be beneficial for both parties, but it often requires additional documentation to ensure a smooth transition. Below are several forms and documents commonly used in conjunction with the Deed in Lieu of Foreclosure.

- Loan Modification Agreement: This document outlines the terms of any modifications made to the original mortgage. It may include changes to the interest rate, payment schedule, or loan amount, allowing the borrower to keep the property under adjusted terms.

- Minnesota Bill of Sale: Essential for documenting the transfer of ownership in Minnesota, this form ensures both parties are protected during the transaction, and additional resources can be found at Formaid Org.

- Release of Liability: This form releases the borrower from further obligations under the mortgage after the Deed in Lieu of Foreclosure is executed. It is essential for protecting the homeowner from future claims related to the mortgage debt.

- Property Inspection Report: This report provides a detailed assessment of the property's condition. Lenders often require this document to evaluate the property's value and determine any necessary repairs before accepting the deed.

- Settlement Statement: Also known as a HUD-1 statement, this document outlines all financial transactions related to the transfer of the property. It details any outstanding fees, credits, and the final amounts due from both parties.

Each of these documents plays a crucial role in the Deed in Lieu of Foreclosure process. They help clarify the terms of the agreement and protect the interests of both the homeowner and the lender. Understanding these forms can facilitate a smoother transition and reduce potential complications during the process.

Misconceptions

Many homeowners facing financial difficulties may consider a deed in lieu of foreclosure as an option to avoid the lengthy and stressful foreclosure process. However, there are several misconceptions surrounding this form that can lead to confusion. Here are seven common misunderstandings:

- A deed in lieu of foreclosure eliminates all debt. Many people believe that transferring the property back to the lender cancels all outstanding mortgage debt. In reality, this may not always be the case. Depending on the agreement, the lender might still pursue a deficiency judgment for any remaining balance.

- It is a quick and easy process. While a deed in lieu can be faster than foreclosure, it is not always simple. Homeowners must meet specific criteria, and lenders will conduct a thorough review before accepting the deed.

- All lenders accept deeds in lieu of foreclosure. Not every lender is willing to accept this option. Some may prefer to go through the foreclosure process instead. It's essential to check with your lender to understand their policies.

- This option is available to everyone. Homeowners must meet certain conditions to qualify for a deed in lieu. For example, they typically need to be in default on their mortgage and unable to sell the property. Lenders will evaluate each situation individually.

- A deed in lieu of foreclosure does not affect credit scores. This misconception can be misleading. While it may be less damaging than a foreclosure, a deed in lieu will still impact your credit score negatively.

- You can choose this option at any time. Many believe they can initiate a deed in lieu at any point in the mortgage process. However, it is usually considered only after all other options, like loan modification or short sale, have been exhausted.

- It absolves you from all legal obligations. Even after a deed in lieu is executed, homeowners may still have legal obligations, especially if there are other liens on the property. It’s crucial to understand what liabilities remain after the transfer.

Understanding these misconceptions can help homeowners make informed decisions about their options when facing financial hardship. Always consider consulting with a legal professional to navigate these complex situations effectively.

Preview - Deed in Lieu of Foreclosure Form

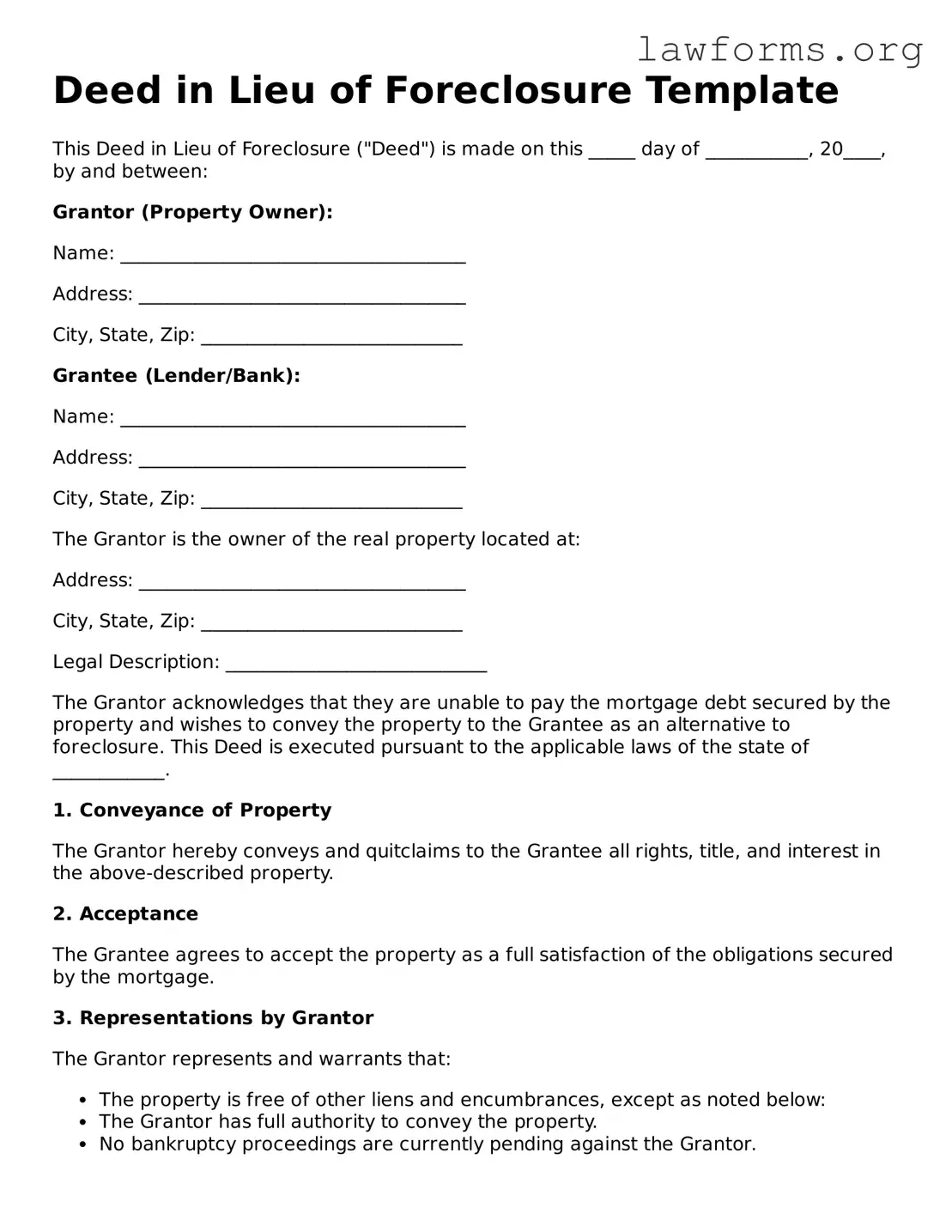

Deed in Lieu of Foreclosure Template

This Deed in Lieu of Foreclosure ("Deed") is made on this _____ day of ___________, 20____, by and between:

Grantor (Property Owner):

Name: _____________________________________

Address: ___________________________________

City, State, Zip: ____________________________

Grantee (Lender/Bank):

Name: _____________________________________

Address: ___________________________________

City, State, Zip: ____________________________

The Grantor is the owner of the real property located at:

Address: ___________________________________

City, State, Zip: ____________________________

Legal Description: ____________________________

The Grantor acknowledges that they are unable to pay the mortgage debt secured by the property and wishes to convey the property to the Grantee as an alternative to foreclosure. This Deed is executed pursuant to the applicable laws of the state of ____________.

1. Conveyance of Property

The Grantor hereby conveys and quitclaims to the Grantee all rights, title, and interest in the above-described property.

2. Acceptance

The Grantee agrees to accept the property as a full satisfaction of the obligations secured by the mortgage.

3. Representations by Grantor

The Grantor represents and warrants that:

- The property is free of other liens and encumbrances, except as noted below:

- The Grantor has full authority to convey the property.

- No bankruptcy proceedings are currently pending against the Grantor.

4. Miscellaneous

This Deed shall be binding upon and inure to the benefit of the parties and their respective successors and assigns. If any provision of this Deed is determined to be unenforceable, the remaining provisions shall remain in effect.

5. Governing Law

This Deed shall be governed by, and construed in accordance with, the laws of the state of ____________.

Signatures

Grantor: _____________________________________ (Signature)

Date: ________________________________________

Grantee: _____________________________________ (Signature)

Date: ________________________________________

Witness: _____________________________________ (Signature)

Date: ________________________________________

Notary Public: ________________________________

My Commission Expires: ______________________

Key takeaways

Filling out and using the Deed in Lieu of Foreclosure form can be a significant step for homeowners facing financial difficulties. Below are key takeaways to consider:

- Understanding the Purpose: A Deed in Lieu of Foreclosure allows a homeowner to voluntarily transfer ownership of their property to the lender to avoid foreclosure.

- Eligibility Criteria: Not all homeowners qualify. Lenders typically require proof of financial hardship and may assess the property's value.

- Impact on Credit Score: While a Deed in Lieu is less damaging than a foreclosure, it can still negatively affect your credit score.

- Legal Advice: Consulting with a legal professional can provide clarity and ensure that all implications are understood before proceeding.

- Documentation Required: Homeowners must gather necessary documents, including proof of income, mortgage statements, and any correspondence with the lender.

- Negotiation with Lender: Homeowners should be prepared to negotiate terms with the lender, which may include forgiveness of remaining debt.

- Future Housing Options: After a Deed in Lieu, finding new housing may be more challenging, as some landlords may view it similarly to a foreclosure.

Understanding these key points can help homeowners navigate the process more effectively and make informed decisions regarding their financial futures.

Similar forms

- Short Sale Agreement: This document allows a homeowner to sell their property for less than what is owed on the mortgage. Like a deed in lieu of foreclosure, it helps avoid foreclosure by transferring ownership to the buyer.

- Loan Modification Agreement: This agreement alters the terms of an existing loan to make it more manageable for the borrower. It can prevent foreclosure by keeping the homeowner in their property.

- Forebearance Agreement: This document temporarily suspends or reduces mortgage payments. It provides relief to homeowners facing financial difficulties, similar to how a deed in lieu aims to resolve mortgage issues.

- Settlement Agreement: This legal document resolves disputes between parties, often involving debt. It can help homeowners negotiate terms with lenders, similar to a deed in lieu.

- Quitclaim Deed: This document transfers ownership of property without guaranteeing that the title is clear. It can be used in situations where a homeowner wants to transfer property rights, akin to a deed in lieu.

- Warranty Deed: This document guarantees that the seller has a clear title to the property. While it is more formal than a deed in lieu, both serve to transfer ownership of a property.

- Power of Attorney: This legal document allows one person to act on behalf of another. It can be used in foreclosure situations to manage property decisions, similar to the intent behind a deed in lieu.

Cease and Desist Letter: A vital tool in legal disputes, a Cease and Desist Letter formally requests that an individual or organization cease harmful actions. It's important for protecting one’s rights, and templates can be found at Forms Washington to ensure the document is properly utilized.

- Release of Lien: This document removes a lien from a property, often after a debt is settled. It can clear the way for a smoother transfer of ownership, much like a deed in lieu does.